Unlike generic crypto research assistants, Fere turns market signals into autonomous trading workflows. Agents research opportunities, build trade setups, optimize routes and fees, execute with a wallet, and monitor strategies 24/7 across crypto and Polymarket. Standout features include autonomous Polymarket trading, entry/exit rules, stop-loss controls, execution routing, and lower-cost agent runs.

What's great

The result of deep research made by this agentic AI is mind blowing couple with the fact that the strategies used when making investment will even be corrected if there is any mistake in the prompt given

What needs improvement

It’s not a "set and forget" money printer. While the NLP is sharp, the agents can occasionally be over-eager during high-slippage events. The learning curve isn't about coding anymore, but about learning how to "prompt" your trading intent clearly. It’s a powerful tool for those who understand market fundamentals but want to offload the 24/7 execution to a machine that doesn't sleep or trade on emotion.

vs Alternatives

As a seasoned user who has been navigating the volatile crypto waves with Fere AI for a while now, here is my breakdown.

Fere AI has genuinely shifted how I approach automated trading. The standout feature is the autonomous agent architecture—it’s a massive leap from the rigid "if-this-then-that" bots of the past. Being able to type out a strategy in plain English and watch the agent interpret market sentiment and cross-chain data to execute it is impressive. I’ve found it particularly effective on the Solana and Base networks, where speed is everything.

Ratings

Ease of use

Reliability

Value for money

Customization

Report

93 views

What's great

deep research capabilities (1)polymarket (2)

Comparing the research against ChatGPT Deep Research on Thinking Extended, AskSurf, Minara, the answer of FereAI stands out in terms of correctness and accuracy.

The ease to apply Limit Orders on Prediction Markets like Polymarket, Kalshi etc is remarkable. This is something no one else has.

Market Pulse gives very real time pulse of everything happening in crypto

What needs improvement

Add more prediction markets - Kalshi

Add HyperLiquid Support

Add AI Enabled trade suggestions

vs Alternatives

ChatGPT by OpenAI

ChatGPT by OpenAI Minara

Minara AskSurf

AskSurfAccuracy and Correctness much better than competition

Ease of Product Usage and ability to do quick actions

Ratings

Ease of use

Reliability

Value for money

Customization

Report

135 views

What's great

polymarket (2)ai-driven investment strategies (2)

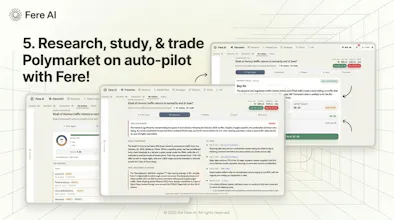

Hey PH, I'm one of the builders at Fere. We're building an autonomous AI agent for crypto and prediction markets — you hand it a thesis in plain English, it does the research, takes the trade, and manages the position itself. I could pitch the whole thing, but I wanna talk about two of my favourite features we shipped:

Polymarket: Prediction markets are the most underrated corner of crypto right now and, every other UI just dumps thousands of markets on you and walks away. We run AI analysis on each market — what the resolution actually hinges on, the catalysts, where consensus odds look mispriced against the underlying signal — and put trade signals right next to it. So the path from "huh, interesting" to "I have a position" is one click instead of three tabs and a gut check. I use it myself daily, which is the honest test.

Strategies: This one is where I let the agent off the leash. I write a rule in plain English — "rotate into the top 5 AI tokens by weekly volume, cut anything down 20%, cap positions at 25% of portfolio" — and it just runs. No Pine Script, no bot dashboard, no babysitting. What's underrated about it: we let you iterate fast — tweak sizing, change entry logic, see how it behaves — and the agent carries context across runs instead of starting from zero. Closest thing I've used to a quant intern who doesn't sleep (so I can).

Ratings

Ease of use

Reliability

Value for money

Customization

Report

121 views

Fere AI

"Your AI should be making your trades, not just narrating them."

That line wouldn't leave us alone. So here we are.

I'm Aron. Pranav and I have been building autonomous AI since 2014, before agents were a buzzword. Enterprise AI for pharma, Fortune 100 ops, web3 infra. Multiple exits. A few brutal failures. One obsession throughout: AI that actually acts, not just answers.

Crypto handed us the perfect environment. But the workflow was broken. I was bouncing between six tabs every morning, and every "AI" I tried would research beautifully then hand me back the mouse. Not an agent. A fancy search engine.

The market splits into two failures:

Chatbots that walk you through a trade and never make it

Bots that fire orders all day and can't tell you why

Either way, you end up doing the work anyway. Fere is the third thing.

Tell it your thesis in plain English. It researches, trades, manages risk — with its own wallet, across multiple chains, for days unattended.

What you can hand it today:

→ "Track top 5 AI tokens by 7-day volume. Rebalance weekly. Cut anything down 20%, let winners run."

→ "Find me easy wins on polymarket"

→ "Every day buy 10$ of eth for me as long as it is under 2400$"

Why it works: most "AI agents" tap out after one prompt. Ours have been live 90+ days straight — reasoning, remembering, adapting, improving. Not scripts with vibes. Real system underneath: planner, retriever, analyst, executor, guardian.

Where we are: 7,000+ daily users. 10M+ autonomous executions. Backed by Ethereal Ventures, Galaxy Vision Hill, and Kosmos Ventures.

We're just getting started. Swarm framework goes open-source next. The agentic internet is coming — we're building the infrastructure early.

Try free at fereai.xyz , no card needed.

What's the trade or thesis you'd actually trust an AI to run? Drop it below 👇 Pranav and I are here all day.

~ Aron & Pranav

The Polymarket integration is what got me.

You claim that most prediction market tools just surface odds while Fere actually trades them autonomously...

Curious how the agent decides which markets are worth entering. Is it purely signal-based or does it factor in liquidity and market depth too? Because thin markets on Polymarket can move fast once a position opens.

@0xaron would love to understand the edge here vs. just trading spot crypto.

Fere AI

@0xaron @abhiranjan_mehta Great question, and you've identified exactly the nuance that makes Polymarket interesting and tricky at the same time.

The agent doesn't just chase odds. Before entering a market, it evaluates signal strength, liquidity depth, and spread, thin markets with wide spreads get filtered out because the slippage kills the edge before you even open the position.

The edge vs. spot crypto is in the structure of the market itself. Polymarket resolves on real-world outcomes - so the signal layer is fundamentally different. You're not reading price action, you're reading information asymmetry. When the agent finds a market where public odds haven't caught up to what the data suggests, that's the entry.

It's a different muscle than spot trading. Took us a while to get the workflow right, but it's one of our favorite things we've built.

Fere AI

@lakshminath_dondeti You’re right that some frontier model providers’ terms/policies treat finance as a sensitive or high-risk domain. But I don’t think the clean reading is “financial or crypto research / trade is prohibited.”

OpenAI’s policy calls out “tailored advice that requires a license” and “automation of high-stakes decisions” in “financial activities and credit,” not financial research broadly. Anthropic is even more explicit: finance is a “High-Risk Use Case,” including investment advice and financial eligibility/creditworthiness, but the requirement is human review and disclosure rather than a blanket ban. Google’s policy has the same general shape around high-risk finance decisions.

Our product follows all standard guidelines for such high risk use case, including disclosures, risk understandings and warnings at necessary steps.

Regarding our choice of models - It varies. We do use the top models in both open and closed weights across different places.

@lakshminath_dondeti @pranavprakash Fair on the policy reading - finance is high-risk-with-conditions, not banned. But the more interesting question your "across different places" answer skips: where in the loop does the actual trading decision get made? An agent that uses closed-weights for research/summarization but open-weights for the trade signal is a very different product from one that pipes positions and signals into a third-party API. The first owns its alpha. The second rents it. Which one is Fere?

Fere AI

@lakshminath_dondeti @ishu86 Its the former. It's a lot sophisticated flow, which deserves a blog post of it's own. The alpha is owned by us. In our case it's our harness, data and context engineering which ensures all the governances, policies, planning and context is correct. We have benchmarked and found same class of models performing exactly same on our platform. So models (in same category) are commodity and can be replaced with open-closed weight ones. So for example - we can switch b/w Sonnet 4.6 and Qwen 3.6 without changing our inferences.

@lakshminath_dondeti @pranavprakash hm makes sense; curious about the benchmarks you are using - have you made them in-house or using some publicly available ones. If the former, would love some takeaways from that work

Question for the team - is leverage trading on the roadmap?

The execution-first approach makes a lot of sense for spot and prediction markets. But the real unlock for an autonomous agent feels like perps and leverage, where speed and signal quality actually compound.

A lot of AI trading tools stop at spot because leverage adds complexity. Curious if Fere is going there or deliberately staying away from it.

Fere AI

@suyash_kr You're thinking about it exactly the way we do.

Short answer: yes, we're going there.

Longer answer: we're actually launching our AI Quant next week - your personal quant trader that lets you build and run your own strategies, not just use ours. Swing and day trading strategies are already live, and we're seeing a 79% win rate on BTC, ETH, and SOL.

On perps specifically, Hyperliquid integration is built. Not publicly live yet, but it's coming very soon.

We didn't stop at spot because it was easier. We stopped there first because getting execution right on spot is the foundation.

Leverage on top of a shaky execution layer is just a faster way to blow up.

The foundation is solid. Perps are next.

Building agents myself, the hardest unsolved problem isn't capability; it's reliability over long horizons.

What's your approach to handling task drift and error recovery in multi-step flows? This is where most agent products silently fail.

Fere AI

@ishu86 This is the right question and most people are not asking it yet.

Task drift and silent failure in multi-step flows is genuinely the hardest infrastructure problem we deal with. Our approach has three layers.

First, specialist sub-agents. Instead of one general agent trying to hold context across a long horizon, each sub-agent owns a narrow, well-defined task. Smaller scope means less surface area for drift.

Second, ordered task execution with checkpoints. Fere breaks a strategy into a sequence of atomic tasks. Each step validates its own output before passing to the next. If something looks off, it does not silently proceed.

Third, live market feedback as a correction signal. Because our agents operate with real wallets in real markets, they get continuous ground truth. Reinforcement learning against live outcomes means errors surface fast and the agent self-corrects over time rather than compounding mistakes.

We will not claim we have fully solved this. Nobody has. But 10 million live executions across 90 plus day strategies gives us a real feedback loop that most agent products running on synthetic benchmarks simply do not have.

Would love to compare notes on what you are seeing on your end.

@abh3nav Agree on decomposition and checkpoints. Want to press on "RL against live outcomes" though, since that phrase covers four very different systems:

Gradient-based online weight updates from live rewards (hard behind closed APIs, risky on open-weights with real capital).

Gradient-based offline fine-tuning on aggregated rewarded trajectories.

Gradient-free in-context learning, past outcomes retrieved into the prompt.

Gradient-free bandit or search over a frozen-weight strategy space.

Each has very different scaling properties and failure modes. Which is Fere actually running? 10M executions is a great corpus for (2) and (3), but it is a different system from a self-correcting policy in the RL sense.

Fere AI

@ishu86 Fair challenge, and you are right to press on it.

We are not running gradient-based online weight updates in production with live capital. That would be reckless and we will not pretend otherwise. What we are running is closest to a combination of (3) and (4) with a pathway toward (2).

In practice: past execution trajectories, including outcomes, slippage, timing errors, and strategy drift signals, are retrieved into context to inform current agent decisions.

Simultaneously, we are running strategy-level selection across a frozen-weight space, where the bandit logic scores and routes to approaches that have performed better on similar market conditions historically.

The 10M execution corpus is exactly what feeds this. We are actively building the offline fine-tuning pipeline on top of it, which is where (2) comes in over time.

Where we are careful with language: self-improving in our context means the system makes better decisions as the corpus grows, not that weights are updating in real time. That distinction matters and we should probably be more precise about it publicly.

This is a genuinely useful push. The RL framing in AI products is often loose and we are not immune to that. Appreciate you making us be specific.

Is there a mode where it suggests trades but waits for your confirmation before executing? Would love to start there before going fully autonomous. Great product either way.

Fere AI

@vishalmehta8340 Not exactly in the way you described but we thought about this a lot.

A confirmation-before-every-trade mode sounds great on paper, but the token cost per decision makes it genuinely impractical at scale. We'd either have to charge a lot more or the agent would be too slow to be useful.

What we do instead: you can backtest and simulate your strategy first. Run it, see how it performs historically, get confident in it, and then flip it to live execution. Same outcome, without the overhead.

And for users who don't want to build their own, our pre-built strategies have been tested and have been delivering consistently. You're not flying blind either way.

As more Fere agents trade the same Polymarket signals, how do you stop your own execution flow from killing the alpha in thin markets?

Fere AI

@sinchana_v Sharpest question of the day and one we've thought about a lot.

A few things work in our favour here.

First, Polymarket markets are outcome-based not price-based. The alpha isn't in being faster than other traders, it's in reading information that hasn't been priced into the odds yet. That's a fundamentally different dynamic from spot crypto where crowded signals kill returns quickly.

Second, we don't route all agents into the same market at the same time. Liquidity and spread are first-class filters. If a market is too thin to absorb position flow without moving the odds against us, the agent doesn't enter. We'd rather miss the trade than cannibilise it.

Third, and honestly the more important answer: as the user base scales, signal diversity scales too. Different users, different risk appetites, different strategy configs. Not a monolithic flow.

The crowding problem is real in quant. We're just not as exposed to it as a pure price-signal product would be.