Launching today

Infinite Bagholder

Pluggable, local-first developer harness for agentic trading

3 followers

Pluggable, local-first developer harness for agentic trading

3 followers

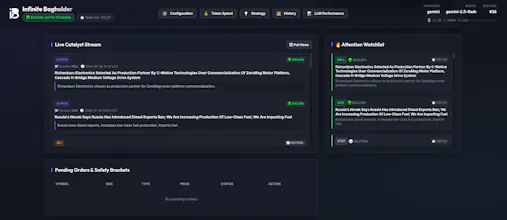

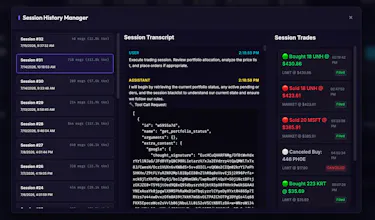

Infinite Bagholder is an open-source, self-hosted Python framework for LLM-powered stock trading on Alpaca and similar brokerages. It provides a local web dashboard to monitor execution logs and agent reasoning in real time. Rather than relying on prompts to enforce risk boundaries, it runs programmatic Python guardrails (like stop-losses and allocation limits) locally before orders are dispatched. Includes a pluggable system for custom news feeds, brokerages, and tools.

Hi Product Hunt,

I’m Ricky, the developer behind Infinite Bagholder.

Let’s be honest: discerning the signal-to-noise ratio of the current discourse around autonomous trading agents is an exercise in futility. You’ve probably seen the pitches promising hands-off wealth generation via API keys and system prompts. In practice, putting an LLM in direct control of an active trading account without a leash is a recipe for a rapid margin call. Models hallucinate, APIs drop requests, and LLMs are notoriously bad at basic math.

I built Infinite Bagholder because I thought the world needed a local sandbox that handles the administrative plumbing (event loops, state management, and logging) while keeping the model under strict, programmatic constraints.

It is a self-hosted Python framework built on FastAPI and SQLite (WAL). It shifts the focus of algorithmic trading away from complex codebase maintenance and toward clear logic. By expressing trading strategies in "plain English" Markdown, developers and quantitative traders can write, run, and test logic without building database tables or handling API loops.

Key Features:

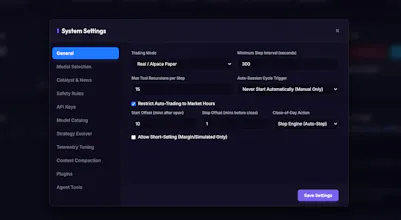

User-Configurable Safety Envelopes: Orders are validated against local Python limits (specified through user settings) before they are ever dispatched to the Alpaca API. If the model hallucinates an invalid symbol or size, the local framework rejects it immediately.

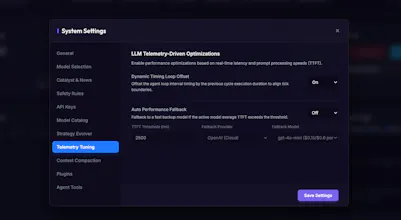

Closed-Loop Strategy Evolution: Includes a dedicated evolution module. You can feed past session transcripts, transaction history, and net P&L/API costs back into a secondary LLM. The system analyzes its own execution history, generates a written critique, and automatically refines the Markdown strategy prompt to optimize performance over time.

Quantitative Inputs: Rather than asking the LLM to calculate indicators, a local technical engine computes Relative Volume (RVOL), SMAs, and Volume Z-Scores and feeds them to the model as structured parameters.

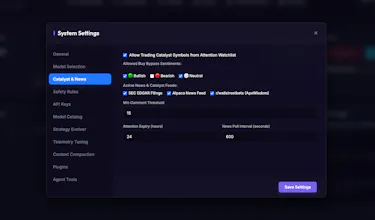

Modular Plugin Interface: Extensible via abstract base classes, allowing you to drop in custom news parsers (e.g. SEC filings), alternate brokerages, or custom tools without touching the core code.

Simulated Execution: A built-in mock broker lets you dry-run strategies offline to inspect the model's decision logs before risking paper or live capital.

Comprehensive Documentation: The repository includes a fully-featured documentation site built by Mkdocs and hosted by Github pages. Aside from a comprehensive codebase reference, this documentation includes ongoing case studies in agent psychology, prompt engineering, and other goodies.

The codebase is open source under the GNU AGPLv3. I’d love to hear your thoughts on the architectural implementation or how you are structuring local agent workflows. I’ll be in the comments to answer questions!

Took it for a spin this weekend and the local dashboard made it easy to watch my agent talk itself out of a trade in real time. The Python-based risk guardrails feel way more reliable than trusting prompts to behave.

The decision to enforce risk limits in actual Python code instead of hoping the LLM listens to a prompt is exactly the kind of pragmatic engineering this space needs. Big fan of the local-first dashboard too.