Launching today

RLX Backtester

Fast Rust backtesting engine for quantitative traders

4 followers

Fast Rust backtesting engine for quantitative traders

4 followers

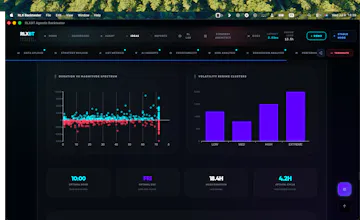

RLX Backtester is a native macOS app built for AI-powered quantitative research. Connect Claude, Cursor, or any MCP-compatible agent to design, backtest, optimize, and stress-test trading strategies locally. Unlike traditional backtesting tools, RLX combines a high-performance Rust engine, reinforcement learning workflows, and an AI-native interface that lets autonomous agents iterate on strategies in real time. Free tier included, with Pro for unlimited research.

How does the RLX engine handle walk-forward validation versus simple in-sample fitting, especially when the reinforcement learning loop starts overfitting to historical regimes?

@gkegjn9

"Great question. The RLX engine handles this through a combination of strict walk-forward cross-validation (WFCV) and deterministic policy freezing:

### 1. Walk-Forward Validation vs. In-Sample Fitting

• Sliding/Anchored Windows: Instead of a single train/test split, the engine runs walk-forward analysis ( walk_forward tool) across multiple rolling windows. The model

(whether rules-based or a neural policy) is optimized/trained strictly on an In-Sample (IS) window and then executed on an adjacent, completely unseen Out-of-Sample

(OOS) window.

• Walk-Forward Efficiency (WFE): We evaluate robustness using the WFE metric:

Average OOS Return

WFE = ──────────────────

Average IS Return

If WFE is close to or above 1.0, the edge is robust. If it decays significantly (e.g., below 0.5), the system flags the configuration as overfitted to local

volatility/trend regimes.

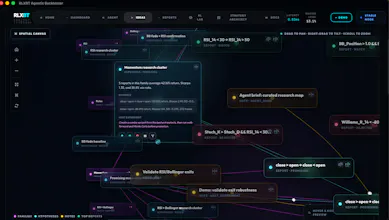

### 2. Preventing Reinforcement Learning Regime Overfitting

When using the RL engine (e.g., DQN or Actor-Critic):

• Deterministic Policy Evaluation: During training, the RL agent uses stochastic actions (via ε-greedy or entropy-regularized policy distributions) to explore. However,

during validation and walk-forward OOS testing, the policy is frozen and evaluated deterministically using the argmax of policy logits. All exploration noise is

disabled.

• Non-Stationary State Space Normalization: To prevent the neural network from memorizing nominal price levels (which leads to regime overfitting), the RLX engine

processes inputs through statistical normalization. Features are converted into stationarity-adjusted metrics such as return z-scores ( ret_z_24 ), drift scores, and

Shannon price entropy. This forces the model to generalize patterns of market structure rather than specific historical price zones.

• Benchmark Comparison: The engine benchmarks OOS performance directly against passive Buy & Hold and randomized baseline agents to ensure that the RL model is capturing

actual alpha rather than riding beta or overfitting to a specific market direction."

Love the MCP integration angle, this feels like the right direction for quant tools right now. One thing I'd really want to see is a built-in walk-forward analysis mode that splits data into rolling in-sample and out-of-sample windows automatically, instead of just a single train/test split. Would make the RL workflow feel a lot more trustworthy out of the box.